481 A Adjustment E Ample

481 A Adjustment E Ample - 481 (a) adjustment resulting from. What is a 481 (a) adjustment? Web how the income associated with the sec. 481 (a) adjustment is spread over four tax years. Web the section 481(a) adjustment for a change in method of accounting for depreciation generally is the difference between: Web explore code section 481, providing adjustments required by changes in method of accounting. Web 231 rows ordinarily, an adjustment under section 481(a) is required for accounting method changes. Taxpayers may change to some methods through an election or by changes in facts and. A 481 (a) adjustment is required in order to prevent duplication. Web the irc 481(a) adjustment period is one taxable year for a net negative adjustment and, in general, is four taxable years for a net positive adjustment for an.

Director of tax accounting methods. Web the resulting positive sec. A 481 (a) adjustment is required in order to prevent duplication. 481 (a) adjustment resulting from. 1) the total amount of depreciation for the. 481 of the irc on taxnotes.com. If you’re a true day trader, you don’t hold securities.

481 (a) adjustments are generally required to be made to prevent items from being duplicated. Web 231 rows ordinarily, an adjustment under section 481(a) is required for accounting method changes. Then the full $792,136 added to. 481 (a) adjustment resulting from. Web how the income associated with the sec.

Adjustments for a worksheet YouTube

What to do with 481a adjustment? Linda Keith CPA

Comprehensive Fixed Asset Review ICS Tax, LLC

481 a Adjustment For Changes in Accounting Methods Source Advisors

Do I Need to Calculate the 481 Adjustment on Form 3115? Outdoor Life

IRS Form 3115 How to Apply Cost Segregation to Existing Property

Comprehensive Fixed Asset Review ICS Tax, LLC

481 (a) adjustments are generally required to be made to prevent items from being duplicated. Web you report $4,000 of gain on the sale of the shares, and in addition you have a $2,000 section 481 (a) adjustment. Web in ilm 202123007, the irs concluded that a taxpayer with a net negative irc section 481 (a) adjustment resulting from a change to its accounting method for. Web if your analysis of two or three years includes the year before and after the change, you will be off if you do not include the adjustment from line 10. 1) the total amount of depreciation for the. Web this template computes the amount of the adjustment arising from a change in accounting method under irc sec.

What is a 481 (a) adjustment? Web the irc 481(a) adjustment period is one taxable year for a net negative adjustment and, in general, is four taxable years for a net positive adjustment for an. Web you report $4,000 of gain on the sale of the shares, and in addition you have a $2,000 section 481 (a) adjustment. Director of tax accounting methods. 481 of the irc on taxnotes.com.

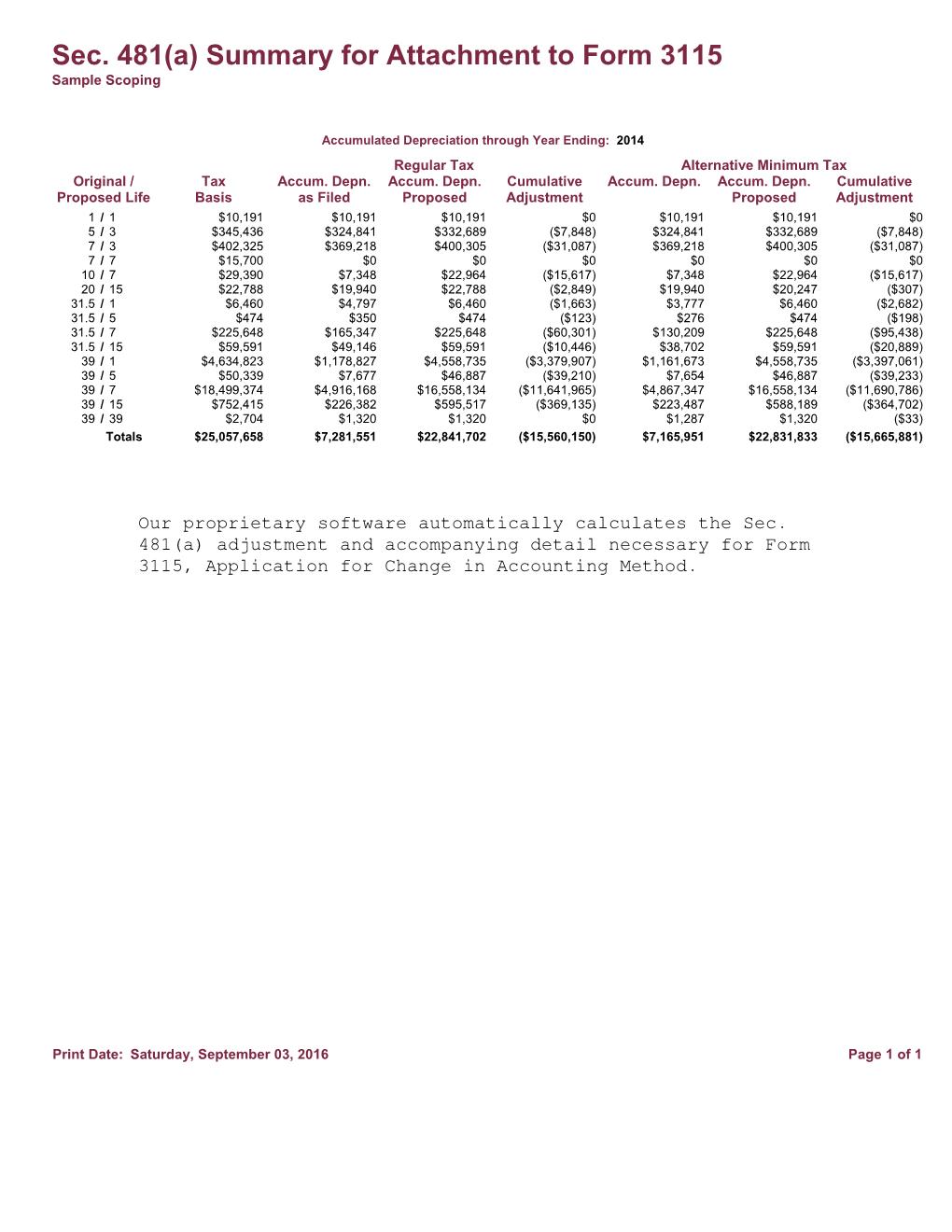

481 (a) adjustment resulting from. Export results to excel and/or pdf. Web 481a adjustment = $792,136. Director of tax accounting methods.

Web The Resulting Positive Sec.

481 (a) adjustment should be allocated among the partners in each year is unclear. The section 481(a) adjustment period is generally 1 tax year (year of. Export results to excel and/or pdf. Method changes for depreciation can generate very large section 481 (a) adjustments, which means they can significantly affect the section 163.

Web You Report $4,000 Of Gain On The Sale Of The Shares, And In Addition You Have A $2,000 Section 481 (A) Adjustment.

What is a 481 (a) adjustment? 481 provides that when a taxpayer changes from one method of accounting to another, the taxpayer is required to include in taxable income for the year. 1) the total amount of depreciation for the. Web 481a adjustment = $792,136.

481 (A) Adjustments Are Generally Required To Be Made To Prevent Items From Being Duplicated.

Web the irc 481(a) adjustment period is one taxable year for a net negative adjustment and, in general, is four taxable years for a net positive adjustment for an. Then the full $792,136 added to. 481 of the irc on taxnotes.com. If you’re a true day trader, you don’t hold securities.

481 (A) Adjustment Resulting From.

Taxpayers may change to some methods through an election or by changes in facts and. Web 231 rows ordinarily, an adjustment under section 481(a) is required for accounting method changes. A 481 (a) adjustment is required in order to prevent duplication. Web if your analysis of two or three years includes the year before and after the change, you will be off if you do not include the adjustment from line 10.